Thank you for your inquiry.

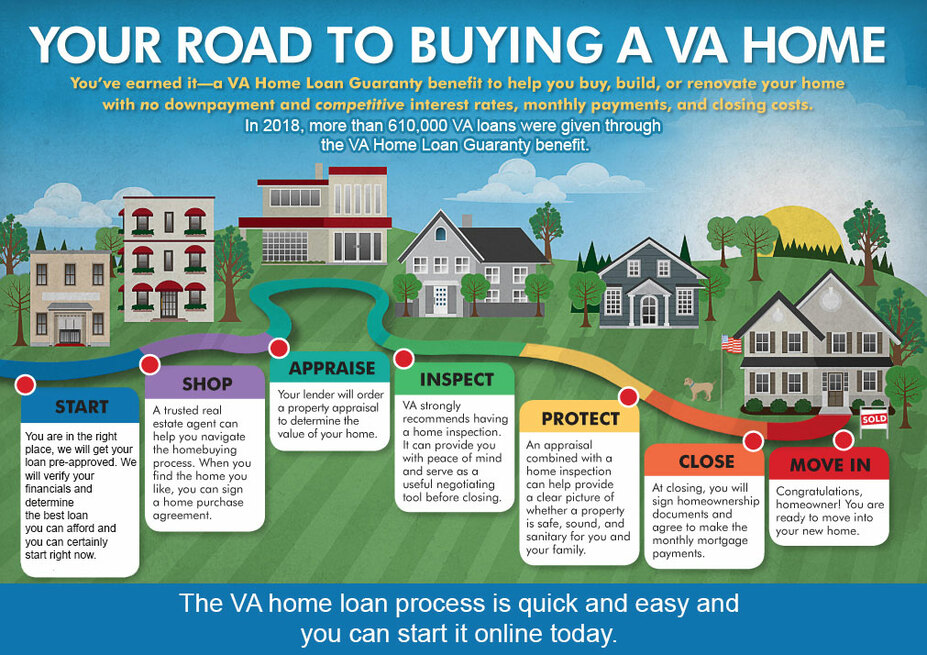

In 2018, more than 610,000 VA loans

were given through the VA

Home Loan Guaranty benefit.

If you are a Veteran you may be eligible

for a broad range of programs and services provided by the Department of Veterans Affairs (VA).

How Does a VA Loan Work?

- A VA home loan is a mortgage that is guaranteed by the U.S. Department of Veterans Affairs

- They are issued by private lenders that are approved by the VA

- The VA does not offer loans, we do

- The VA will guarantee your loan

- VA loans do not require a down-payment

- You can finance 100% of the price of the home

- Military service persons and their spouses may be eligible

- Mortgage insurance premiums (PMI) is not required

- VA funding fee of 2.15% for first-time buyers or 3.3% for repeat buyers is needed

Who is Eligible?

Basic VA Service Eligibility Requirements:

Basic VA Service Eligibility Requirements:

- 90 days of consecutive active duty service

- More than 180 days of active duty service during peacetime

- 6 or more years in the National Guard or Reserves

- Active-duty Military

- Cadets of the U.S. Military, Coast Guard Academy, or Air Force

- U.S. Naval Academy Midshipmen

- Atmospheric and National Oceanic Administration officers

- U.S. Public Health Service officers

VA Credit Score Requirements

- VA home loans technically don’t have a minimum credit score

- The Department of Veterans Affairs may guarantee a mortgage loan regardless of your FICO scores

- We may be able to approve credit scores of 580 and higher

- We will look at more than just your FICO score

- We will take into account your entire credit history

- FHA loans are also available for those with lower credit scores

- If you have a credit score below 580 we will help you improve your credit score before applying

- If you have at least a 10% down payment you may qualify for an FHA loan with a credit score as low as 500

|

|